Jul 17, 2026 / By Vanessa Horwell

9 min read

SHORT TAKE: The Fourth of July cost more than ever this year, and Americans reached for credit, BNPL, and AI-assisted checkout tools to bridge the gap. Economics aside, what does that say about the state of payments, and the fintech brands meeting consumer demand for affordability?

This year’s Fourth of July celebrations felt a little off. Actually, a lot off. Maybe it was the weight of the country’s 250th anniversary on the metaphorical shoulders of a divided citizenry. Maybe it was the fact that most of my friends were more interested in watching France squeak by Paraguay in the World Cup than schlepping in the heat to a local Independence Day parade. Maybe it was the heat itself; even in Miami, where we’re no strangers to summer sweltering, the Bayfront Park fireworks were delayed until midnight on account of the weather.

Or maybe it was the sheer cost of, well, everything.

Take my neighbors’ experience on the fourth. Their plan was to go to the beach in the morning to beat the crowds and the heat, then host a cookout in the afternoon before fireworks in the evening – a perfectly typical American Independence Day routine. They bought a new cooler for the occasion, not a fancy Yeti or anything, just a sturdy replacement for their old Igloo, but one that set them back $50 anyway. Parking at the beach is always $20, and they had to gas up their SUV to get there. And then the obligatory stop at Publix for BBQ supplies.

I don’t know exactly what they spent that day, but it was clearly enough to reach for a credit card. It was a topic of conversation while watching the France-Paraguay match.

And I’ll bet that across the country, friends and neighbors were having similar conversations over grilled hot dogs, canned beer and international soccer. Because that is the shape of consumer pricing, spending and payments in 2026.

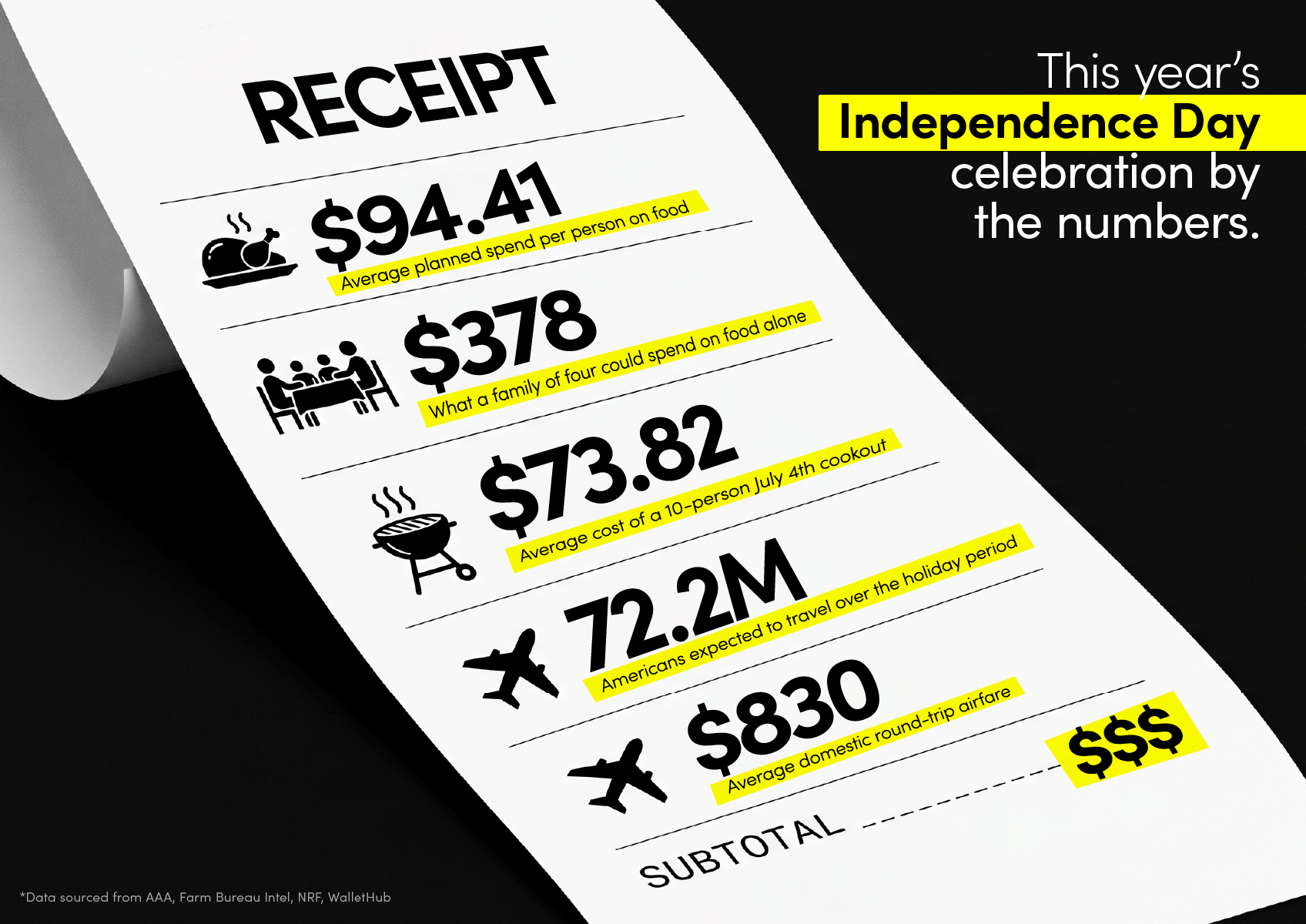

Americans planned to spend a record $94.41 per person on food alone for Independence Day this year, according to the National Retail Federation, or about $378 for a family of four before anyone bought fireworks, gas, or ice. Total holiday food spending topped $9.4 billion. The American Farm Bureau Federation put the average cost of a classic cookout for 10 at $73.82, the highest since it started tracking the number in 2016.

Those are just the stay-at-home figures. AAA projected 72.2 million Americans would travel over the holiday, with domestic round-trip airfare averaging roughly $830 per person, meaning a family of four flying to see grandparents in Denver was staring down more than $3,300 in tickets before they picked up a rental car.

It’s an expensive time to be an American, and we’re hungry for payment products that help us spread the cost.

When The Cookout Costs A Car Payment

The Fourth of July is a useful shorthand for what has happened to household budgets, because every American who fires up a grill or drives to see fireworks at the park gets a real-time itemized receipt of how much more expensive the same afternoon has become.

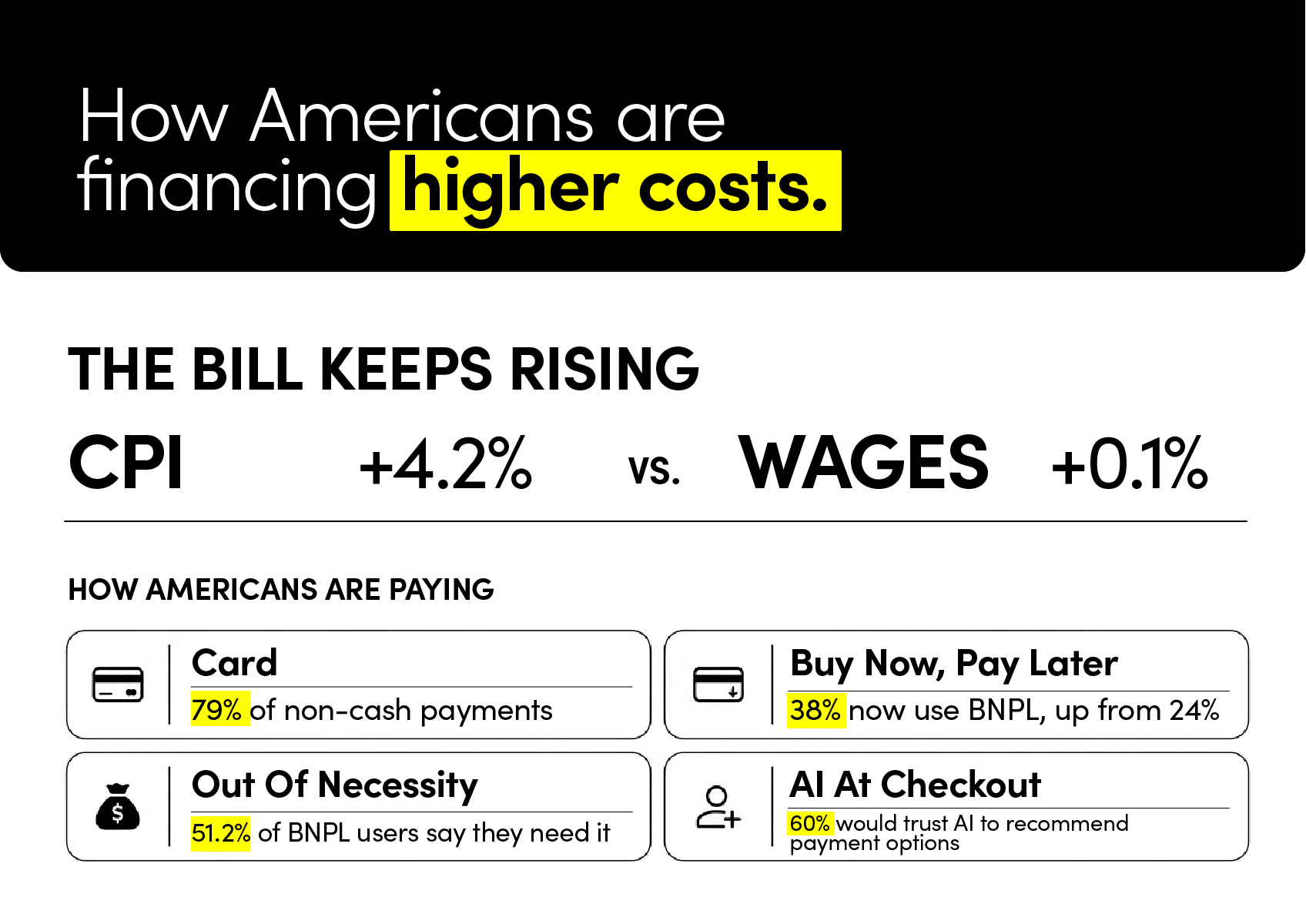

The latest Bureau of Labor Statistics bulletin put the Consumer Price Index up 4.2% year-over-year in May 2026, the largest 12-month jump since April 2023. Energy prices rose 23.5% over the same period. Households know this without reading the news release; they feel it at the grocery store checkout, at the gas pump, and in the moment their kid asks for one more sparkler or toy, and they do the math on the drive home.

The cash in their checking account did not grow to match. Real, inflation-adjusted wages grew just 0.1% over the year ending March 2026, according to the BLS Employment Cost Index. The differential between prices and available funds has created an appetite for alternative payment tools—and an opportunity every marketing and product lead in payments and fintech can’t afford to ignore.

Why Consumers Are Reaching For Different Tools

Americans are reshuffling their payment methods to spread costs across time and across products. The Federal Reserve Payments Study, published in June, found that card payments accounted for 79% of noncash payment volume in 2024, up from 77% in 2021. Driving that shift is the fact that credit card payments grew more than debit card payments for the first time in any measured three-year period since 2000.

The Fed is positioning that as an anomaly, but it sure seems like a structural change. For most of the last two decades, debit was the default payment rail for everyday spending. Consumers used their own money, drew it down against a paycheck, and reached for credit only when a larger purchase warranted it. Credit outpacing debit growth means households are now financing more of the everyday basket, from groceries to gas to the replacement beach-day cooler. Is that a good thing?

Buy Now, Pay Later has followed the same affordability-driven trend. PYMNTS Intelligence, in its 2025 "Pay Later Revolution" study, found that BNPL usage jumped from 24% of American consumers in 2023 to 38% by late 2024, putting it on par with general-purpose credit cards. More than half (51.2%) of adult BNPL users say they use it out of necessity, not convenience. Six in 10 hold multiple active BNPL loans at the same time.

Consumers want help navigating the current payment environment. The PYMNTS Intelligence and Splitit "Pay Later Ecosystem" report published in June found that more than six in 10 shoppers would consider letting AI recommend Pay Later options at checkout, provided the recommendation protects their credit score, surfaces the cheapest option, and leaves the final call in their hands. Gen Z and millennials lead that adoption. They already use AI to compare plans, monitor credit, and manage budgets, and they see no reason for the checkout page to be an exception.

What This Means For The Payments and Fintech Industry

None of these numbers add up to a story that ends quickly

Real wages remain flat. Grocery prices sit roughly 25% above 2019 baselines, according to USDA Economic Research Service analysis of BLS Food-at-Home CPI data. Energy prices are running double-digit annual increases and fluctuate with the tides in the Strait of Hormuz. Tariff policy (yes, this is still a thing) is unlikely to ease pressure on the price of goods that Americans buy at retail. Housing, insurance, and healthcare costs continue to rise faster than the general index. The structural factors squeezing household spending power in 2026 are not the kind that resolve inside a single election cycle or a single quarter of Fed policy.

That means the shift in payment behavior is probably here to stay. Credit balances will keep growing. BNPL will keep expanding, both to necessity users looking for a bridge and to convenience users looking for control. AI-assisted checkout tools will move from novelty to expectation. And the demand for products that let consumers spread costs, compare options in real time, and avoid credit pitfalls will keep rising alongside them.

For fintechs and payment technology companies, that creates opportunities if they can position themselves as leaders in helping consumers pay in ways that reflect how they live. That means flexible installment products that fit the purchase, transparent AI-driven recommendations that keep the user in control, and underwriting that acknowledges the reality of stacked loans without punishing borrowers for using the tools designed for them.

Our neighbors that hosted us at their Fourth of July cookout surely logged into their bank apps on Monday morning to find out exactly how much the weekend cost (or maybe they didn’t want to). They might then have wondered what tools were available to help them spread that cost. Payment brands that offer those tools with credibility and clarity will earn the checkout button when the next holiday, or even when the next Tuesday grocery run rolls around.

How is affordability reshaping the way your customers’ customers pay? Start a conversation with us about the content your buyers need.

Want more PAYMENTS insights? Check out these resources